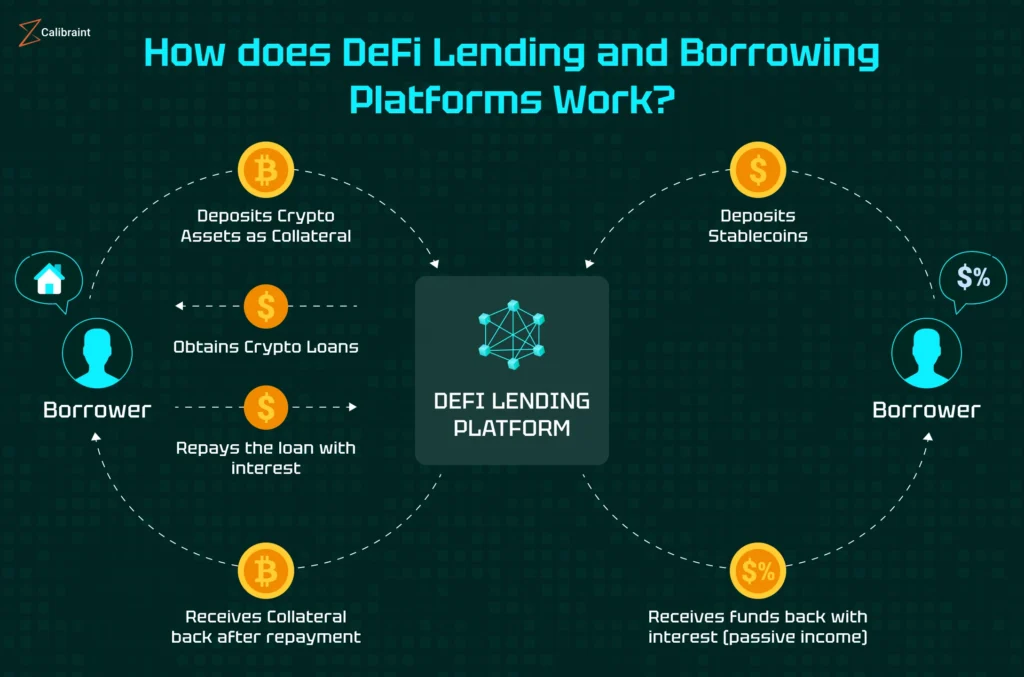

DeFi lending is a class of protocols where loans are issued without bank paperwork: terms are enforced by smart contracts, and repayment is secured through overcollateralization and liquidations. This lets users unlock liquidity without selling their assets, but it requires strict risk control (LTV/health factor) and a clear understanding of market parameters.

How DeFi Loans Work

Deal Participants

- Lenders (suppliers) — deposit assets into a pool/market and earn interest. Rates are driven by borrowing demand and available liquidity.

- Borrowers — post collateral, borrow another asset (often a stablecoin), pay interest, and manage liquidation risk.

Why the Protocol Can Operate Without Trust

- Loans are typically overcollateralized: collateral value exceeds debt.

- Smart contracts strictly cap borrow limits and enable liquidations when a position becomes unsafe.

- Prices come from oracles; many protocols use averaged pricing (e.g., TWAP) to reduce manipulation risk.

Why Lending Matters: Unlocking Capital Without Selling

The core use case is obtaining liquidity while keeping exposure to the asset (i.e., not realizing a sale). This can be useful when you want temporary capital for other operations but prefer not to exit your base position. The cost of that flexibility is interest expense and liquidation risk during market stress.

Collateral and Limits: Why Assets Differ

What Determines How Much You Can Borrow

- Collateral volatility: higher volatility usually means lower limits (more conservative parameters).

- Liquidity: thinner markets increase the risk of poor liquidation execution.

- Price feed quality: oracle reliability, update frequency, and resistance to manipulation.

- Stress behavior: how the asset and its markets behave during sharp moves.

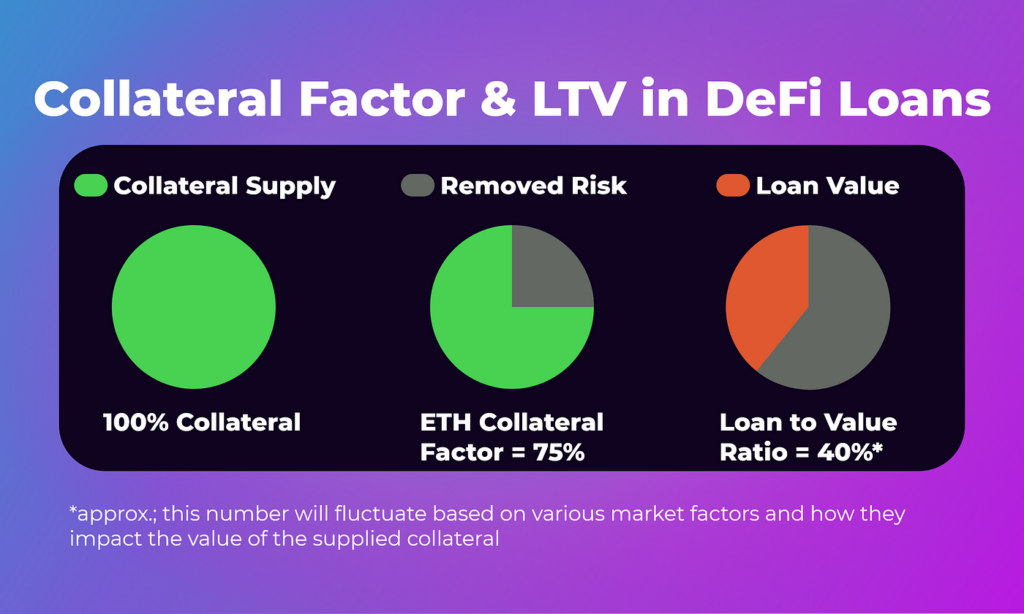

As a result, each market defines a set of risk parameters: max LTV, liquidation threshold, and liquidation bonus (sometimes with additional fees).

LTV, Liquidation Threshold, and Liquidation Bonus

LTV: Debt-to-Collateral Value Ratio

LTV (Loan-to-Value) shows how tightly you are utilizing collateral:

LTV = (debt value) / (collateral value)

- LTV increases if collateral price drops, the borrowed asset appreciates, or interest accrues.

- The closer LTV gets to the critical level, the higher the liquidation risk.

Liquidation Threshold: The Liquidation Trigger Level

The liquidation threshold is the LTV level at which a position becomes liquidatable. This is the key red-line metric for risk management.

Liquidation Bonus: Incentive for Liquidators

The liquidation bonus is the economic incentive for liquidators (a discount/bonus on collateral) to ensure liquidations happen quickly even in stressed markets. For borrowers, it effectively increases the cost of being liquidated.

Comparison Table: LTV vs Threshold vs Bonus (Risk Logic)

Below are typical ranges (for intuition, not protocol-specific numbers) to illustrate how parameters map to risk:

| Collateral Profile | Example (Conceptual) | Max LTV (Borrow Limit) | Liquidation Threshold (Critical) | Liquidation Bonus | What It Means for Borrowers |

|---|---|---|---|---|---|

| Conservative | majors / “blue-chip” assets | 70–80% | 75–85% | 4–8% | Higher borrow capacity, but you still need a buffer—especially in volatile markets |

| Medium risk | liquid altcoins | 50–70% | 60–75% | 6–12% | Wider risk zone: LTV rises faster with price moves; liquidations are more common |

| High risk | volatile tokens / “long tail” | 20–50% | 30–60% | 10–20% | Liquidation is closer and more expensive; without a large buffer risk is high |

| Stablecoins as collateral | stable-collateral | 80–90% | 85–95% | 1–5% | Risk often shifts to depegs/oracles/system events rather than volatility |

How to read it: a higher threshold allows more risk utilization; a higher bonus improves liquidation efficiency for the protocol but increases borrower liquidation costs.

How Liquidation Works

Liquidation Trigger

A position becomes liquidatable when LTV reaches the liquidation threshold (as determined by oracle pricing). To reduce manipulation, many protocols use averaged prices (e.g., TWAP).

The Liquidator’s Role

- The liquidator repays part of the borrower’s debt.

- They receive part of the collateral with a bonus (liquidation bonus).

- They realize profit as compensation for risk and speed.

What the Borrower Keeps (and Loses)

- Upside: the debt is reduced or fully repaid.

- Downside: a portion of collateral is sold/seized during adverse market conditions, plus bonus/fee friction.

How to Estimate the Liquidation Price (Theory)

A simplified model (to understand mechanics):

C— amount of collateral,P— collateral price,D— debt (in $),T— liquidation threshold.

Liquidation becomes possible when:

D / (C * P) >= T

Liquidation boundary price:

P_liq = D / (C * T)

Intuition: more debt brings liquidation closer; more collateral pushes it farther away; a more conservative threshold triggers liquidation sooner.

DeFi Lending Risks: Beyond Price Moves

📍 Smart Contract Risk

- code vulnerabilities,

- economic attacks,

- integration risks (pools, bridges, external modules).

📍 Oracle Risk

- feed outages or delays,

- price manipulation in thin markets,

- “false” liquidation events.

📍 Liquidity Risk in Stress Markets

- slippage increases,

- market depth drops,

- liquidations become more painful.

📍 Parameter/Governance Risk

- changes to max LTV, threshold, or bonus,

- moving an asset to stricter modes (e.g., isolation),

- risk policy changes at the protocol level.

Checklists

Borrower Checklist (Risk Management)

- ✅ I understand what asset my debt is denominated in and how its price affects LTV.

- ✅ I am not borrowing at the limit; I keep a buffer in LTV/health factor.

- ✅ I know the liquidation threshold and can estimate my liquidation price.

- ✅ I understand the liquidation bonus/fees and the real cost of liquidation in my market.

- ✅ I have assessed the oracle (reliability, update cadence, manipulation resistance) and protocol design.

- ✅ I have a plan for stress scenarios (sharp moves/gaps) and know how I will respond.

Lender Checklist (Supplier Risk)

☑️ I understand yield is dynamic and depends on borrowing demand.

☑️ I account for smart contract risk (audits are not guarantees).

☑️ I understand how the protocol handles risky assets and liquidations (including bad debt scenarios).

☑️ I evaluate system dependencies: oracles, liquidators, and DEX/CEX liquidity.

FAQ

1. What matters more for liquidation risk: max LTV or liquidation threshold?

For liquidation risk, the key parameter is the liquidation threshold. Max LTV affects the initial borrow cap, but liquidation is defined by the threshold.

2. Why do liquidations happen at the worst possible time?

They are triggered by sharp price moves and deteriorating liquidity: markets get thinner, slippage rises, and liquidation friction increases.

3. Is the liquidation bonus a protocol fee?

Typically, it’s an incentive paid to liquidators (funded by borrower collateral via a discount). Some protocols also charge separate fees.

4. Why do protocols use TWAP/averaged pricing?

To reduce the impact of short-lived price spikes and make manipulations that trigger liquidations harder.

5. Can liquidation risk be eliminated entirely?

Not entirely: extreme scenarios (gaps, depegs, oracle issues) still exist. But keeping a buffer in LTV and choosing more robust collateral/markets can significantly reduce the probability.