Decentralized finance (DeFi) was once hailed as a transformative force capable of reshaping global finance. Built on transparency, automation, and permissionless access, the sector promised to dismantle traditional banking barriers. However, as the industry progresses through 2026, that early optimism is being tempered by a more critical assessment of its underlying economic structures.

While blockchain technology remains powerful and innovative, many DeFi protocols still rely on fragile financial models. Without a transition from internal speculation to real-world utility, the long-term relevance of the ecosystem is increasingly being questioned.

Recursive Lending Dominates the System

One of the most significant weaknesses in DeFi lies in its circular lending structure. Unlike traditional finance, where loans typically fund productive activities such as business expansion or infrastructure, DeFi lending often revolves around recycling capital within the system.

Users deposit volatile crypto assets, borrow stablecoins, and frequently reinvest those funds back into the same assets. This creates leverage loops that amplify gains during bullish conditions but fail to generate real economic value. As a result, yields are driven more by speculative demand than by productive output.

Inflationary Tokenomics and Short-Term Liquidity

Many DeFi platforms depend on liquidity mining programs that reward users with newly issued governance tokens. While this approach can attract rapid capital inflows, it often results in “mercenary liquidity” — investors who quickly move funds to whichever protocol offers the highest returns.

Because these tokens frequently lack strong utility, their value is highly dependent on continued demand. When market sentiment shifts, token prices decline, yields drop, and liquidity exits rapidly. This dynamic has repeatedly led to sharp collapses in protocol stability.

Over-Collateralization Limits Real Adoption

Another structural limitation is the reliance on over-collateralized lending. Borrowers are required to lock up more value than they receive, which restricts access to those who already hold significant capital.

This model excludes individuals and businesses that actually need financing, particularly in emerging markets. Instead of enabling broader financial inclusion, DeFi often ends up serving well-capitalized traders and speculators.

Liquidation Cascades Increase Market Volatility

Automated liquidations, while essential for protocol solvency, can amplify systemic risk. When collateral values drop, smart contracts trigger forced sales. In volatile conditions, this can lead to cascading liquidations that push prices even lower.

These feedback loops have historically resulted in rapid market downturns, eroding billions in value within short periods and exposing the fragility of interconnected DeFi systems.

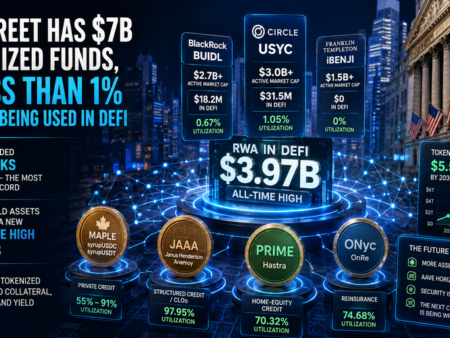

Real-World Assets Offer a Path Forward

To achieve long-term sustainability, DeFi must expand beyond closed crypto-native economies. Integrating real-world assets (RWAs) — such as government bonds, trade finance instruments, and private credit — introduces external sources of yield.

This shift can provide more stable and predictable income streams, reducing dependence on speculative activity. It also aligns DeFi more closely with traditional financial markets, increasing its appeal to institutional investors.

On-Chain Credit Systems Reduce Collateral Dependence

The development of decentralized identity and on-chain credit scoring could significantly transform lending models. Technologies like zero-knowledge proofs allow users to demonstrate creditworthiness without exposing sensitive data.

This innovation opens the door to undercollateralized lending based on financial history rather than locked assets, potentially enabling access to credit for real businesses and individuals worldwide.

Modular Architecture Improves Risk Management

Modern DeFi protocols are increasingly adopting modular designs that isolate risk. Instead of relying on shared liquidity pools, newer systems separate markets to prevent failures from spreading across the entire platform.

This approach reduces systemic contagion and enhances overall resilience. Combined with improved security practices and insurance mechanisms, it makes the ecosystem more robust and better suited for institutional participation.

Cultural Shift Is Essential for Sustainability

Beyond technical improvements, DeFi must also undergo a cultural transformation. The industry’s reputation for high-risk speculation and unsustainable yields continues to deter mainstream adoption.

A shift toward risk-adjusted returns, transparency, and long-term value creation is necessary. Regulatory clarity will also play a crucial role, providing the legal certainty needed for businesses and investors to operate confidently within the space.

Conclusion

DeFi remains one of the most innovative sectors in finance, but its next phase will depend on meaningful structural change. Moving away from speculative loops and toward real economic utility is essential for long-term growth.

By integrating real-world assets, developing credit-based lending systems, and improving protocol design, DeFi can evolve into a more stable and inclusive financial ecosystem. Without these changes, however, the industry risks stagnation as yields decline and speculative interest fades.