Decentralized finance (DeFi) is facing a major reality check in 2026 as yields across leading protocols fall below returns offered by traditional financial platforms. Once seen as a high-reward alternative to banks, DeFi now presents a difficult equation: higher risk with lower returns.

At its core, DeFi enables users to lend, borrow, and trade assets directly on blockchain networks without intermediaries. During the 2021–2022 boom, this model attracted billions in capital by offering double-digit—and sometimes triple-digit—annual yields. Today, that advantage has largely disappeared.

DeFi vs Traditional Finance: The Yield Gap Narrows

One of the clearest signs of this shift is the comparison between DeFi lending rates and traditional brokerage accounts. Aave, currently the largest DeFi lending protocol by total value locked (TVL), offers around 2.6% APY on USDC deposits. Meanwhile, platforms like Interactive Brokers provide approximately 3.1% on idle cash balances.

While the difference may appear small, it fundamentally challenges DeFi’s value proposition. Investors are now exposed to smart contract risks, exploits, and liquidity shocks—without receiving a meaningful premium in return.

This dynamic has not gone unnoticed. Market participants increasingly question whether DeFi’s risk-reward balance still makes sense in a low-yield environment.

What Happened to DeFi’s High Yields?

Just a few years ago, DeFi yields were significantly higher. In 2024, protocols like Ethena attracted massive inflows by offering yields exceeding 40% APY through token incentives and complex trading strategies.

However, those returns proved unsustainable. As incentives dried up and market conditions normalized, yields rapidly declined. Ethena’s APY has since dropped to roughly 3.5%, while its TVL has fallen sharply from peak levels.

Across the broader ecosystem, similar trends are visible:

- Stablecoin lending pools on Aave now yield between 1.8% and 2.5%

- Liquid staking assets such as stETH offer around 2.5%

- Most major pools struggle to exceed 3% APY

The key reason is simple: DeFi yields today are primarily driven by organic borrowing demand rather than token incentives. With reduced leverage and weaker market sentiment, demand for borrowing has declined—dragging yields down with it.

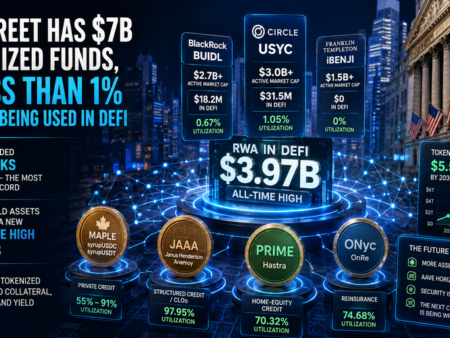

Real-World Assets Are Propping Up Returns

Some DeFi platforms still offer higher yields, but many rely on exposure to real-world assets (RWAs). For example, certain stablecoin savings products generate returns above 3.5% by allocating capital to U.S. Treasuries, institutional lending, or centralized reward programs.

While this approach stabilizes yields, it introduces a trade-off. Investors seeking purely on-chain exposure may find that these hybrid models blur the line between DeFi and traditional finance.

This shift raises an important question: if returns are increasingly dependent on off-chain assets, is DeFi still delivering on its original promise?

New Models Aim to Restore Yield

To address declining returns, some protocols are experimenting with new lending frameworks. Platforms like Morpho allow specialized “curators” to create customized vaults with tailored risk parameters and strategies.

This model introduces competition at the strategy level, enabling differentiated yields rather than uniform returns across pooled liquidity. Certain curated vaults are still able to generate yields above 4% or even higher in niche cases.

However, even these innovations fall far short of the explosive yields seen during previous cycles.

Confidence Takes a Hit Amid Exploits and Shutdowns

Yield compression is only part of the problem. Confidence in DeFi has also been shaken by a series of high-profile exploits and protocol failures.

Recent incidents include:

- A $110 million exploit that led to the shutdown of a major decentralized exchange protocol

- A $25 million attack on a stablecoin system caused by missing safeguards rather than code flaws

- More than $2.4 billion in crypto stolen during the first half of 2025 alone

Notably, attackers are evolving. While smart contract code has become more secure, vulnerabilities increasingly stem from operational failures, compromised keys, and social engineering attacks.

For investors comparing a 2–3% DeFi yield with a similar or higher return in traditional finance, these risks weigh heavily on decision-making.

Regulatory Pressure Adds Uncertainty

Beyond market dynamics and security concerns, regulation is emerging as another headwind. Proposed legislation in the United States could restrict passive yield generation on stablecoins, potentially limiting one of DeFi’s core use cases.

If implemented, such rules may push yield generation further into regulated or centralized channels, reducing the competitive edge of decentralized platforms.

The lack of clarity around these proposals adds uncertainty at a time when DeFi is already struggling to maintain momentum.

The Bottom Line: A New Era for DeFi Yield

DeFi is entering a more mature phase where unsustainable incentives are fading, and returns are aligning closer to traditional financial benchmarks. While this may signal long-term stability, it also removes one of the sector’s biggest attractions.

Today, investors must weigh modest yields against persistent risks, including exploits, protocol design flaws, and regulatory changes. The gap between DeFi and traditional finance is narrowing—and in some cases, reversing.

For now, the numbers tell a clear story: the easy yield era is over, and DeFi must evolve to remain competitive in a world where safer alternatives offer similar returns.

FAQ

- Why are DeFi yields falling?

Yields are declining due to reduced borrowing demand, the removal of token incentives, and overall weaker market conditions. - Is DeFi still profitable in 2026?

Yes, but returns are significantly lower than in previous years and often comparable to traditional finance options. - Are higher-yield opportunities still available?

Some exist through specialized strategies or RWA-backed products, but they typically involve additional complexity or off-chain exposure. - Is DeFi riskier than traditional savings accounts?

Yes. DeFi carries risks such as smart contract vulnerabilities, hacks, and liquidity issues that do not apply to insured bank accounts. - Will DeFi yields increase again?

Some analysts believe yields could rise with stronger market activity, but structural changes suggest they may remain closer to traditional rates long term.