Revenue across major decentralized finance (DeFi) lending protocols and decentralized exchanges (DEXs) declined significantly over the past week as traders reduced leverage following the early June market correction. While short-term fee generation fell sharply, industry participants argue the downturn reflects a normal deleveraging cycle rather than any fundamental weakness in the on-chain credit market.

According to data from DefiLlama, several of the largest DeFi protocols experienced substantial declines in seven-day fee revenue. Aave V3, the leading lending platform by total value locked (TVL), recorded a 60% drop in fees to $6.72 million. Morpho Blue also saw fees decline by 60% to $3.27 million, while Maple Finance reported a 59% decrease to $1.25 million.

The downturn extended beyond lending markets. On the trading side, Uniswap V3 generated $3.74 million in weekly fees, down 57% from the previous period, while Curve Finance experienced an even steeper decline of 65%, bringing fees down to approximately $891,000.

Monthly Data Paints a Different Picture

Although the weekly figures appear severe, longer-term metrics suggest the sector remains healthy. Over the past 30 days, fee generation across several major protocols remains significantly higher than earlier levels.

Morpho Blue’s monthly fees increased 23%, Maple Finance posted a 49% gain, Uniswap V3 climbed 27%, and Curve Finance surged 71% over the same period. The contrast between strong monthly growth and weak weekly performance indicates that the recent pullback is more likely the result of temporary deleveraging than a sustained decline in user activity.

Because DeFi lending and trading fees are closely tied to borrowing demand and leverage levels, periods of elevated market volatility often create unusually high revenue. As leverage is removed from the system, protocol utilization and fee generation naturally decline.

Market Normalization After a High-Volatility Period

Industry leaders argue that comparing current fee levels to those generated during the early June selloff creates a misleading narrative. During market crashes, liquidations accelerate, borrowing rates spike, and trading volumes increase dramatically, producing exceptional revenue for lending protocols and exchanges.

Himanshu Sahay, co-founder of fixed-rate lending platform Arch Network, explained that the previous week represented an extraordinary environment rather than a sustainable baseline.

According to Sahay, crash-related liquidations tend to generate elevated fees as leveraged positions unwind. Once markets stabilize and leverage decreases, fee levels return to more normal ranges. He emphasized that fee sensitivity is an inherent characteristic of variable-rate on-chain lending systems, where revenue directly reflects utilization and borrowing demand.

Carry Trade Opportunities Continue to Shrink

Misha Putiatin, co-founder of collateral infrastructure platform Symbiotic, believes the weakness stems from reduced profitability in leverage-based trading strategies.

In both traditional finance and DeFi markets, borrowers are willing to pay interest when they can deploy capital into opportunities that generate higher returns. However, while liquidity remains abundant across the ecosystem, the number of attractive and scalable investment opportunities has decreased.

Putiatin noted that risk appetite has weakened following several recent industry disruptions, including the KelpDAO exploit and the STRC depegging event. As a result, many investors and liquidity providers have become more cautious, reducing demand for borrowed capital.

When lending supply exceeds productive borrowing demand, borrowing costs decline and lending yields compress. This dynamic helps explain why multiple protocols with different business models experienced similar revenue declines during the same period.

Not All Lending Protocols Were Hit Equally

The correction was not universal across the sector. Some protocols demonstrated stronger resilience than others, suggesting that borrower composition and liquidity structure continue to play important roles in performance.

SparkLend recorded a more moderate decline of 20.7%, generating nearly $989,000 in seven-day fees. Euler V2 experienced only a slight decrease of 2.8%, while Compound V3 stood out as the only major protocol to post growth, with weekly fees rising 3.8% to $368,000.

Market observers attribute Compound’s relative strength to its borrower base, which is more heavily focused on stablecoin working-capital strategies rather than speculative leverage. Similarly, SparkLend’s access to DAI-related liquidity may have helped cushion the impact of the broader deleveraging trend.

DeFi Tokens Continue to Rally Despite Revenue Pullback

Perhaps the strongest evidence against a structural crisis is the performance of major DeFi governance tokens. Despite declining protocol fees, investors appear confident that the recent slowdown is temporary.

Over the past week, the AAVE token gained approximately 23%, while UNI, the governance token of Uniswap, advanced around 31%, according to market data from CoinGecko.

The positive price action suggests that traders view the recent revenue weakness as a cyclical adjustment rather than a sign of long-term deterioration within the DeFi sector.

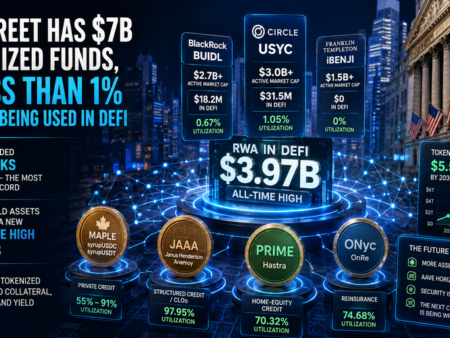

Real-World Assets Could Drive the Next Yield Cycle

Looking ahead, industry executives increasingly see real-world assets (RWAs) as the next major catalyst for sustainable on-chain yield generation.

Jacopo Buriollo, founder and CEO of Megawatt Finance, believes future growth will come from financing productive assets that generate predictable cash flows, including energy infrastructure and other real-economy projects. Unlike speculative leverage cycles, these opportunities can create returns that are linked directly to economic activity.

Putiatin echoed this view, arguing that the DeFi industry is entering a more mature phase where yield generation will increasingly rely on RWAs and other sustainable sources rather than purely speculative borrowing demand.

While the recent drop in protocol fees highlights the sensitivity of DeFi markets to leverage cycles, the broader trend suggests that on-chain credit markets remain intact. As new sources of yield emerge and institutional adoption expands, many industry participants expect the sector to continue evolving beyond its dependence on speculative trading activity.