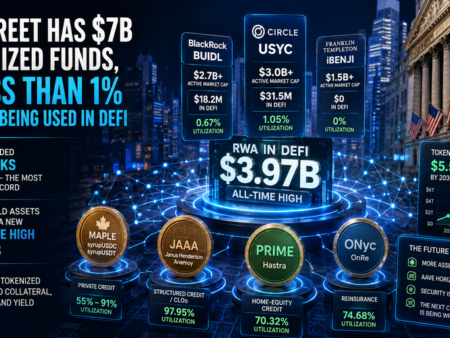

The tokenized real-world asset (RWA) sector is expanding rapidly, approaching a major milestone of nearly $30 billion in on-chain value. However, the majority of this capital remains disconnected from decentralized finance applications. While blockchain-based representations of Treasuries, money market funds, commodities, equities, and private credit continue gaining traction, only a small portion of these assets is actually participating in the broader DeFi ecosystem.

According to data from DefiLlama’s RWA category tracking, roughly $2.47 billion currently appears as active DeFi TVL — assets actively deposited into third-party protocols, collateral systems, and liquidity markets. This means less than 10% of the entire tokenized asset landscape is participating in open DeFi infrastructure.

Billions On-Chain, But Limited DeFi Activity

Different RWA categories display vastly different integration levels with decentralized finance.

| RWA Category | On-Chain Market Value | Active DeFi TVL | DeFi Utilization Ratio |

|---|---|---|---|

| Bond & Money Market Funds | $16.6B+ | $920M | ~5.5% |

| Gold & Commodities | $5.7B | $183.6M | ~3.2% |

| Stocks & Equities | $2.7B | $78.27M | ~2.9% |

| Private Credit | $3.226B | $1.257B | ~39% |

Private credit remains the strongest exception. Protocols such as Centrifuge and Maple Finance were designed around lending structures from the beginning, allowing assets to function naturally inside DeFi environments.

Meanwhile, categories including Treasury products, tokenized gold, and equity offerings were largely built for regulated institutional ownership rather than open blockchain composability.

Permissioned Infrastructure Creates Friction

A key reason for the gap between total RWA growth and DeFi participation comes from how many tokenized assets are structured.

BlackRock’s BUIDL fund illustrates this issue clearly. Although the fund represents one of the largest institutional tokenization efforts, DefiLlama reports only around $18.9 million in active DeFi TVL associated with it.

The reason is architectural rather than technical.

Institutional products frequently include:

- Wallet allowlists and KYC verification

- Transfer-agent reconciliation processes

- Qualified-investor requirements

- Scheduled redemption periods

- Restricted secondary-market access

While these features satisfy regulatory obligations, they create obstacles for permissionless DeFi applications.

| Constraint | Purpose | Impact on DeFi Integration |

|---|---|---|

| KYC / Allowlisting | Restricts ownership to approved users | Limits participation in open liquidity pools |

| Transfer-Agent Verification | Provides legal ownership reconciliation | Reduces smart contract autonomy |

| Qualified Investor Rules | Restricts access to institutions | Excludes retail liquidity |

| NAV Redemption Windows | Uses scheduled settlement periods | Conflicts with real-time DeFi systems |

| Centralized Trading Venues | Keeps activity on closed platforms | Activity remains outside DeFi TVL metrics |

Tokenized Gold Shows Another Side of the Story

The tokenized commodity market adds another layer of complexity.

Tokenized gold trading volumes accelerated dramatically during the first quarter of 2026, reportedly exceeding $90 billion in spot activity and surpassing full-year 2025 totals.

Yet despite strong trading activity, only around $183.6 million appears inside DeFi protocols.

The discrepancy exists because most activity takes place on centralized exchanges and institutional venues rather than within permissionless decentralized applications.

Where Optimism Still Exists

Despite structural barriers, several projects demonstrate that tokenized assets can successfully integrate into decentralized ecosystems when composability becomes a design priority.

Examples include:

- USDY: surpassed $1 billion TVL while expanding across nine blockchain networks

- Morpho: accumulated over $620 million in RWA deposits

- Aave Horizon: reached roughly $423.5 million in RWA-related market activity

- Ondo Global Markets: achieved approximately $650 million TVL and over $12 billion cumulative trading volume

These examples suggest that tokenized assets do not necessarily need to sacrifice compliance to achieve DeFi compatibility.

Several industry participants increasingly argue that the market is splitting into two separate models:

- Ownership-first systems: prioritizing regulation and institutional controls

- Composability-first systems: prioritizing secondary liquidity and DeFi utility

The Bearish Scenario: Closed Ecosystems Dominate

Long-term forecasts remain highly optimistic for tokenization overall. Standard Chartered projects tokenized assets could approach $2 trillion by 2028.

However, there is growing concern that much of this growth may remain trapped inside institutional infrastructure rather than flowing into open financial systems.

Research increasingly suggests that isolated compliance structures and fragmented settlement models could create closed liquidity silos rather than interconnected financial networks.

If that happens, tokenization may grow enormously without substantially expanding decentralized finance itself.

Two Markets Hidden Behind One RWA Label

The current numbers reveal that the RWA sector may actually represent two separate industries operating under the same narrative.

The first is regulated on-chain finance, built around institutional products, managed issuance, and tightly controlled access.

The second is DeFi-native composability, where assets function as permissionless collateral, liquidity sources, and programmable financial primitives.

Projects such as Morpho and USDY demonstrate that the second model is gaining momentum, but it remains relatively small compared with the broader market.

For the DeFi participation ratio to rise significantly beyond today’s levels, future token issuers may need to prioritize open circulation and secondary utility during the design process rather than layering compliance restrictions on top of blockchain infrastructure.

For now, most of the nearly $30 billion RWA market still resembles regulated financial infrastructure running on blockchain rails rather than the fully interconnected DeFi economy many originally envisioned.